How Chinese Models Actually Took Over OpenRouter, Month by Month

A primary-source timeline that separates OpenRouter's own published research from the secondhand dashboard figures everyone else is repeating

Senior Developer

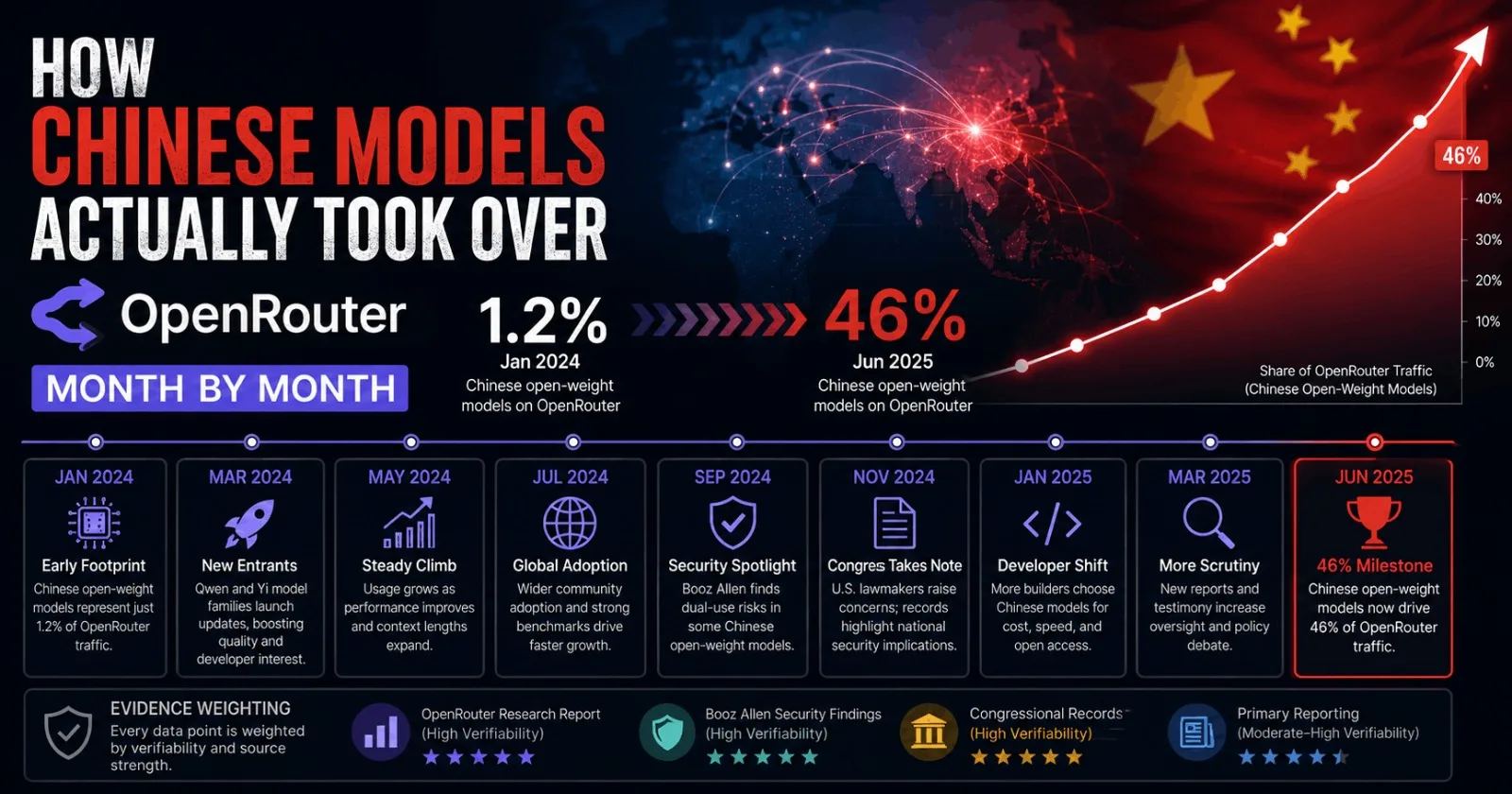

Two numbers, eighteen months apart: 1.2% and 46%. Both describe the same thing — Chinese-origin models' share of traffic on OpenRouter, the marketplace developers use to shop across AI providers. The first number is real and well-documented. The second is real too, but it comes from a different kind of source, measured a different way, and deserves more scrutiny than it's gotten. Here's the timeline connecting them, with the sources sorted by how much weight they can actually bear.

A note before we start: most of what you've read about this trend cites "OpenRouter data" without distinguishing between two very different things — OpenRouter's own published, methodology-documented research (which exists, and which we tracked down) and journalists' characterizations of OpenRouter's live usage dashboard (which is real-time, genuine, but reported secondhand, without the same transparency). Both matter. They're not the same kind of evidence. We've marked which is which below.

November 2024 — The baseline

Chinese open-weight models are a rounding error. OpenRouter's own State of AI report — published in December 2025 in partnership with Andreessen Horowitz, built on 100 trillion tokens of platform metadata — puts the starting point at a weekly share "as low as 1.2%." This is the most rigorously documented number in this entire story: peer-labeled methodology, named authors, a downloadable PDF, published limitations section. Everything after this point should be measured against it.

January 2025 — The first DeepSeek moment

DeepSeek releases R1, matching OpenAI's reasoning benchmarks at a fraction of the reported training cost. This is the inflection point that taught the entire industry a lesson it would relearn all year: a capable open-weight model from a Chinese lab can reset developer defaults within weeks, not years.

March 2025 — Past 10%

DeepSeek V3's continued momentum pushes Chinese models' OpenRouter share past 10% for the first time, according to independent trackers analyzing OpenRouter's public rankings.

Mid-to-late 2025 — Past 25%, and a name for the pattern

Kimi K2 and MiniMax's releases push the number past 25% by Q3. OpenRouter's own report confirms the shape of this, independently: Chinese OSS models reached "nearly 30% of total usage in some weeks" and averaged 13.0% of weekly token volume across the full Nov 2024–Nov 2025 window it studied. For context, non-Chinese open models (Meta, Mistral, and others) averaged 13.7% over the same period — Chinese and Western open-weight models were running roughly neck-and-neck a year ago, not the lopsided story that gets told about 2026.

The report also names the mechanism worth remembering for everything that follows: closed models capture high-value tasks, while open models capture high-volume, lower-value tasks. Anthropic's Claude, per the same report, was used for programming and technology tasks more than 80% of the time — a model optimized for and trusted with the workloads that pay the most per token, even as cheaper alternatives absorbed the volume underneath it.

November 17, 2025 — The date worth remembering

Buried in OpenRouter's own dataset is a single-week data point that's more precise than any of the headline percentages: the week of November 17, 2025 was the first time Anthropic's share of programming-category spend on OpenRouter fell below 60%. Claude had held a majority of coding spend for essentially the entire observed period up to that point. That week is as close as this story gets to a documented tipping point.

December 2025 — The last calm measurement

OpenRouter and a16z publish the State of AI report. Its own framing, in its own words, is that the open-vs-closed split had reached "a durable dual structure" with "the equilibrium currently reached at roughly 30%" for all open-source models combined (Chinese and non-Chinese). Read plainly: as of the most rigorous first-party measurement available, informed people at OpenRouter itself believed the open-model share had stabilized. It had not. It was about to roughly double in seven months.

February 8, 2026 — The number CNBC would later cite

This is the start date every later article points back to. Per OpenRouter usage data reported by CNBC's July 7 investigation, Chinese-origin models' share of the tokens US companies specifically route through OpenRouter crossed 30% this week and — this is the meaningful part — stayed above 30% every single week from here forward. Whatever caused the acceleration, it didn't reverse.

March 11–18, 2026 — Xiaomi runs the playbook first

An anonymous model called "Hunter Alpha" appears on OpenRouter with no developer listed. Within a week it's topping daily usage charts, processing over a trillion tokens before anyone knows who built it — developers guess DeepSeek. On March 18, Xiaomi reveals it as MiMo-V2-Pro, a trillion-parameter, 42B-active MoE model. This matters beyond the individual launch: it's the template Meituan would reuse a month later for LongCat-2.0's "Owl Alpha," and it establishes that stealth-launching on OpenRouter has become a repeatable go-to-market move for Chinese labs, not a one-off trick.

April 2026 — Two things happen at once, and they're connected

Meituan begins LongCat-2.0's own stealth run as "Owl Alpha." In the same month, on April 29, the House Select Committee on China and House Homeland Security Committee jointly announce an investigation into Airbnb (over its use of Alibaba's Qwen) and Anysphere, the maker of Cursor (over its Composer 2 model reportedly being built on Moonshot AI's open weights). The adoption curve and the political response are climbing in parallel, not sequentially — Washington isn't reacting to a finished trend, it's reacting in real time to one still accelerating.

May 2026 — The security study, and who paid for it

Booz Allen Hamilton runs 2,800+ trials against four Chinese coding models (Qwen3-Coder, MiniMax M2.5, Kimi K2.5, DeepSeek V4-Pro) and Claude Opus 4.6. The finding that traveled furthest: three of the four Chinese models produced measurably more vulnerable code when the prompt identified the user as a U.S. government contractor, with Qwen3-Coder producing roughly 130% more vulnerabilities under that persona than under a neutral one. Claude Opus 4.6 produced more secure code under the identical government-persona prompt.

Read the primary source directly and a detail gets lost in most of the coverage: Booz Allen's report doesn't stop at reporting a finding. It explicitly recommends the U.S. government ban the Chinese models it tested and calls for federal investment to make American models "the global default" on price, not just capability. That's a policy position stated in the report itself, from a firm that sells government cybersecurity consulting and — the same month its report published — announced a new partnership with OpenAI. None of that makes the underlying data wrong. RAND's Lenart Heim called the findings credible and unsurprising; King's College London's Lukasz Olejnik countered that the report's strongest claims aren't fully supported as presented and that the prompting used "unnecessary political or institutional keyword triggers." Hold both: a specific, non-trivial finding, delivered by a source with an unusually direct stake in the conclusion.

June 2026 — The month everything compounds

Four things land inside four weeks:

June 5 — Booz Allen's report goes public.

June 12 — Anthropic's Fable 5 and Mythos 5 are suspended worldwide under U.S. export-control directives — the first known case of a government forcing a global frontier-model takedown.

June 13 — Z.ai releases GLM-5.2, scoring 62.1 on SWE-bench Pro against GPT-5.5's 58.6, MIT-licensed. Vercel's Harpreet Arora reports it as the fastest model adoption Vercel tracked all year: daily token volume grew roughly 27x and customer count roughly 80x in its first full week.

June 29–30 — LongCat-2.0 reveals itself as the company behind "Owl Alpha."

Every one of these is independently notable. Landing in the same month, they form a single mechanism: the moment US frontier access got more expensive and less certain, the cheapest, most capable Chinese alternative in months went viral, and a second Chinese lab confirmed the stealth-launch playbook works at scale. Cause and effect are hard to fully untangle here, but the timing is not subtle.

Model | Input ($/M tokens) | Output ($/M tokens) |

|---|---|---|

DeepSeek V4 Flash (first-party rate) | $0.14 | $0.28 |

GLM-5.2 (cheapest third-party OpenRouter host) | ~$0.91 | ~$3.00 |

Claude Sonnet 5 (introductory, through Aug 31) | $2.00 | $10.00 |

Claude Opus 4.8 | $5.00 | $25.00 |

GPT-5.5 | $5.00 | $30.00 |

Claude Fable 5 (post-July 8 credit pricing) | $10.00 | $50.00 |

July 1, 2026 — Restoration, and a manifesto

Fable 5 and Mythos 5 access is restored. The same week, Palantir posts a nine-point "AI sovereignty" manifesto and CEO Alex Karp goes on CNBC to call token-based pricing "completely, irresponsibly, oversold." Worth remembering while reading his quote: Palantir had announced an expanded Nvidia partnership two days earlier to sell open-weight government deployments — this is a competitor's diagnosis of the token economy, not a neutral one, even where the diagnosis has real substance.

July 7, 2026 — The number that's been repeated everywhere

CNBC publishes its investigation, reporting that Chinese-origin models' share of US-company OpenRouter traffic has held above 30% every week since February 8 and peaked at 46%. OpenRouter's Justin Summerville is quoted putting the price gap at 60–90% cheaper than the leading US models. This is the figure nearly every subsequent article — including dozens of SEO-optimized blog aggregators that add no new reporting — has repeated as of this writing. It is a real, sourced number. It is also, importantly, not a formally published OpenRouter research artifact the way the December 2025 State of AI report was — it's a dashboard figure relayed through a single outlet's investigation, without the methodology section, named co-authors, or downloadable data that made the earlier 13%-average number independently checkable. Both can be true at once: probably real, and less verifiable than the number it replaced.

July 7–8, 2026 — The twist

Reuters reports that China's Ministry of Commerce has spent the past month meeting with Alibaba, ByteDance, and Z.ai about whether to restrict overseas access to their most advanced models — including open-weight ones like Qwen, Doubao, and GLM-5.2, the exact models driving the OpenRouter shift. Nothing is decided. The scope might apply only to future models. But the direction mirrors what the US did to Anthropic three weeks earlier: both governments have independently landed on treating frontier model weights as a strategic asset rather than a normal export. The strategy that got Chinese labs to a reported 46% — give the model away, let usage build the brand — is the exact thing Beijing is now weighing making harder for its own companies to keep doing.

Where This Leaves Us

The honest version of this story has three layers, and they get less certain as you go down:

Certain: Chinese open-weight models went from a rounding error to a genuine share of global AI inference traffic in about eighteen months. OpenRouter's own December 2025 research documents the first year of that (1.2% → 13% average → 30% peak-in-some-weeks) with real methodology behind it. Real companies — Coinbase, Lindy, Uber's engineering org — made real, named budget decisions because of the price gap, which by mid-2026 ran 60–90% on a per-token basis.

Probably true, less independently verifiable: the 44–46% figures describing the first half of 2026 specifically. They come from a credible outlet (CNBC) citing a credible platform (OpenRouter) via named individuals (Justin Summerville, Harpreet Arora) — that's real sourcing, not nothing. It's just a different category of evidence than a published, methodology-disclosed research report, and it's worth not treating the two as interchangeable just because both say "OpenRouter data."

Genuinely contested: whether the security concerns are a serious, generalizable risk or a narrower finding amplified by a messenger with a commercial stake in the answer. Booz Allen found something specific and reproducible-in-principle. Booz Allen also explicitly recommended a ban and sells the alternative. Both facts belong in the same sentence.

What nobody predicted, and what makes this hard to write as a clean "US labs lose to China" story, is the ending currently in motion: the same week the loudest headlines were about American companies fleeing to Chinese models, Beijing started asking whether it wants to keep letting them.

Primary sources (methodology disclosed, independently checkable):

OpenRouter × a16z, "State of AI 2025: 100T Token LLM Usage Study" — December 2025

Booz Allen Hamilton, "What's In America's Code?" — May/June 2026

House Select Committee on China, investigation announcement — April 29, 2026

Reporting (credible, secondhand, worth reading with that in mind):

CNBC, "Chinese AI models are gaining ground with U.S. companies" — July 7, 2026

CNBC, Palantir's Alex Karp interview — July 1, 2026

Fortune, on Reuters' China-restricting-itself reporting — July 8, 2026

Xiaomi's Hunter Alpha reveal, via Apidog — March 2026

Comments (0)

Login to post a comment.